Impulsive Spending and ADHD: Why It Happens and What Actually Helps

If you have ADHD and/or struggle with impulsive spending, you are not alone, and you are definitely not “bad with money.”

For many people with ADHD, impulsive spending is only one piece of a much larger financial picture. ADHD can show up financially as stress shopping, buying things impulsively online at night, avoiding bills and mail because they feel overwhelming, forgetting subscriptions, paying late fees, starting budgeting systems that never stick, or emotionally spending money on a “better version” of yourself.

As an Accredited Financial Counselor (AFC®), helping people change impulsive spending behavior is literally my job. Here are some of the strategies that tend to work well, especially for ADHD brains.

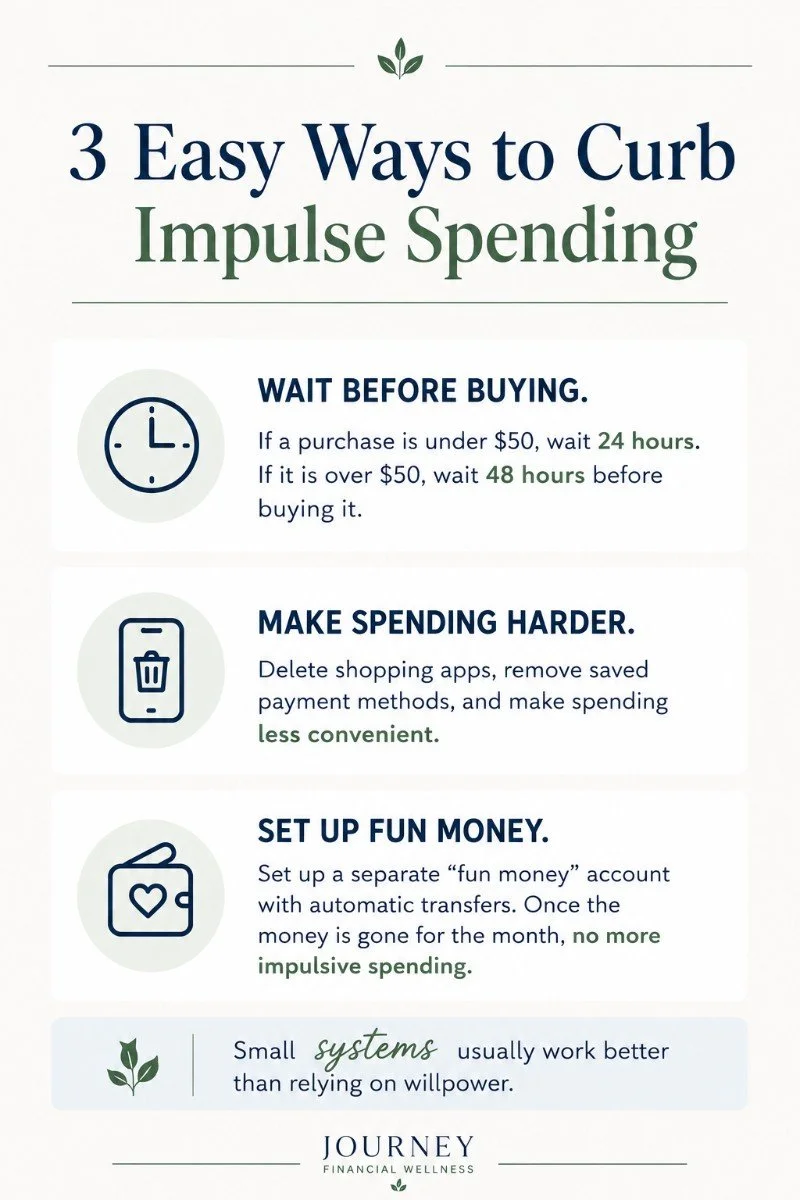

TL;DR? If you're feeling overwhelmed even reading this post, I got you. Start here with these 3 things.

Ready for more? Read on.

None of this is about perfection. It is about building small systems and habits that help you slow down, pause, and make more intentional decisions with your money.

Know Your Goal

A vague goal like “I should save more money” usually is not strong enough to interrupt impulsive spending. Specific goals work much better.

Before making an unplanned purchase, pause and ask yourself:

How does this help me achieve my financial goals?

Am I buying this because I truly value it, or because of a feeling / I want the dopamine hit?

What am I giving up by spending this money?

That last question matters - it’s about tradeoffs. Every dollar spent is a dollar not going toward debt payoff, savings, travel, retirement, freedom, flexibility, or reducing stress later.

This is not about guilt. It is about awareness.

If setting financial goals feels overwhelming, using SMART goals can help make them feel clearer and more achievable instead of vague and stressful.

Related: How to Use SMART Goals for Financial Goal Setting

Wait Before Buying

Impulsive spending feeds off urgency. ADHD brains especially struggle with the feeling that something needs to happen immediately.

Usually, it does not.

The 24-hour rule works because it creates distance between emotion and action. Put the item in your cart and walk away. Screenshot it if you are afraid you will forget. Chances are, a surprising number of those “must-have” purchases will lose their appeal once your nervous system settles down.

Keep the rule simple:

Under $50: wait 24 hours

Over $50: wait 48 hours

People often tell themselves they will miss the sale, but sales come back around constantly. Retailers are counting on you believing this is your only chance.

It almost never is.

Everyone Needs Fun Money

Trying to go from emotional spending to “I will never buy anything fun again” is usually unrealistic and short-lived. Instead, you can plan for it.

Create a line item in your budget specifically for spontaneous or fun spending. The key is making it intentional and affordable instead of chaotic.

One strategy that works really well is setting up a separate checking account just for fun or impulsive spending and automatically transferring money into it each payday.

Once that money is gone for the month, no more spontaneous spending.

That approach creates boundaries without requiring constant self-control, and it removes a lot of the shame spiral people experience around money.

You are not failing because you wanted to buy something fun. You are simply staying within the boundaries you already decided were financially safe.

Make Spending Harder

ADHD and convenience are a dangerous combination when it comes to money. The easier it is to buy something, the more likely you are to do it without fully thinking it through.

Create friction on purpose:

Delete shopping apps

Remove saved credit cards from Amazon, Apple Pay, Google Pay, PayPal, Shop Pay, and retailer websites

Unsubscribe from retailer emails and texts

Log out of shopping websites after purchases

Avoid Buy Now, Pay Later services like Klarna, Afterpay, Affirm, PayPal Pay Later, and Sezzle

You are not trying to make life miserable. You are simply slowing the process down enough for your logical brain to catch up with your emotional brain.

Even small inconveniences can interrupt autopilot spending.

That Thing? It Is Not an Emergency

One of the biggest traps with ADHD spending is that you are often not actually buying the thing. You are buying the fantasy of what the thing represents.

The cute planner that will finally make you organized. The outfit that will make you feel confident at the event. The hobby supplies for the version of yourself that suddenly has endless free time and motivation. The skincare, decor, or gadgets tied to the fantasy of becoming calmer, happier, healthier, more productive, or more put together.

ADHD brains crave novelty and possibility. That creates a powerful pull toward the “what if?” version of ourselves.

But after the package arrives, reality kicks in. Now you have to clean it, organize it, store it, use it, maintain it, and often deal with the guilt or shame that follows when it gets tossed in a doom pile. That dopamine spike fades quickly.

The reality of whatever urgency ploy, countdown clock, or sale is popping up in your feed? Most things are not rare opportunities. Most things come back in stock. Most trends disappear in six months. Most purchases feel far less exciting after a little time passes.

The urgency is usually emotional, not factual.

And honestly, social media has made this much worse. People are constantly being sold the idea that their life is one product away from finally being organized, productive, attractive, calm, successful, or fulfilled.

That is marketing, not reality. Hyped trends come and go. These are not investments, just stuff.

Try to shop for the life you are actually living and building, not the fantasy version of your future self.

And before you buy anything, wait 24 hours. The 24-hour pause matters because it gives that dopamine spike time to settle. Most of the time, you were not actually after the thing itself. You were after the feeling attached to it.

Time = Money

Instead of thinking, “It’s only $80.”

Ask yourself, “How many hours did I have to work to earn that $80?”

Money is not just numbers in your bank account. It represents your time, energy, stress, focus, and labor. Reconnecting purchases to real effort (blood, sweat, and tears, even) helps many people become more thoughtful about spending decisions.

Stop the Debt Cycle

This is the hard truth nobody wants to hear. You cannot consistently pay down debt while continuing to create new debt. You must stop using credit cards in order to pay off debt.

If credit cards are fueling impulsive spending, it may help to temporarily move to:

Debit card only

Cash only

One emergency credit card

Freezing or locking cards

Removing cards from digital wallets

This means you switch to only spending funds in your account that are allocated for that purchase. This is not punishment; it's a reset. It is creating guardrails while you take time to build healthier habits and regain control.

Because the reality is, paying 20-35% interest on impulsive purchases creates stress that lasts far longer than the dopamine hit did.

Track It Without Shame

A lot of people with ADHD avoid looking at their finances because it feels overwhelming, emotionally loaded, or embarrassing. But avoiding the numbers usually increases anxiety, not decreases it. Fear of the unknown, right?

A notebook and pen. Excel sheet. Or, use an app that makes tracking simple and visual:

Quicken Simplifi

Monarch Money

Rocket Money

Perfection is not the goal, awareness is.

You cannot improve what you refuse to look at, but you also do not need a perfect system to make meaningful progress. Perfect is the enemy of good enough.

Pause and Ask Why

Sometimes people with ADHD are not buying products as much as they are buying relief from overwhelm, stress, boredom, insecurity, or emotional discomfort.

Before buying something impulsively, pause and get to the root of the feeling. Ask:

Am I stressed?

Bored?

Avoiding something?

Looking for comfort?

Trying to become a “better version” of myself overnight?

Am I buying this for the life I actually have, or for the fantasy version of my life?

You do not need to fully solve the emotional reason in the moment. Just pausing to notice the source or pattern can help interrupt mindless spending.

And if certain spending habits feel emotionally loaded or difficult to control, that may be something worth exploring through journaling, coaching, or therapy.

Fix Your Environment

If your social media feed constantly encourages spending, overconsumption, and comparison, it is going to affect your behavior - whether you realize it or not.

Delete social media apps from your phone if they trigger spending. Charge your phone across the room at night. If you rely on your phone as an alarm, consider getting an old-school alarm clock instead. Unsubscribe from marketing emails. Really, just look away.

Reducing exposure to constant marketing can make a bigger difference than people expect.

Unfollow accounts that make you feel inadequate or constantly tempted to buy things. Follow people who model positive behaviors, encourage intentional living, mindful spending, budgeting, decluttering, or realistic financial habits instead.

Final Takeaways

Impulsive spending is not fixed through shame, guilt, or beating yourself up every time you buy something unnecessary. Most people already feel bad enough! What actually helps is creating systems, boundaries, awareness, friction, and intentional habits that work with your brain instead of against it.

Be gentle on yourself. Honestly, progress matters a lot more than perfection.

You do not need to become someone who never spends money on fun things. You just need spending decisions to become more thoughtful than automatic.

That is a skill, and it can absolutely be learned.

Ready for more? How to Stop Compulsive Shopping for Good